How Long Do Negative Items Stay on Your Credit Report?

A credit score is the credit information – your credit history determining your credibility as a borrower to the lender. Moreover, it is crucial for credit cards approval, (some) employments, and various other factors we’ll be discussing later.

From pre-pandemic debts and credit issues to post-pandemic revenge spending in Canada, there are myriad whys and wherefores Canadians (and nearly everybody) need to take care of credit repairs and credit restoration to maintain a healthy credit file.

Today mortgages, auto dealerships, credit cards, and loan approvals are accessed after passing the reliability test – the credit score condition – which represents how elegantly (or unintelligently) you have been utilizing your credit.

Why Credit Score is Crucial?

Creditors evaluate the risk of lending (to you) by your credit report. Following are some of the many factors deciding your credit score and your financial obligation situation:

- Payment history – Do you clear bills/ loan installments in time?

- Age of the accounts you have

- Balances

- The types of accounts you have

- The number of credit inquiries

Credit Score Range

There are five distinct categories when evaluating the credit score:

| Poor credit score | 300-574 |

| Below Average credit score | 575-659 |

| Fair credit score | 660-712 |

| Good credit score | 713-740 |

| Excellent credit score | 741-900 |

Poor Credit Score:

If you have a poor credit score, try to improve your credit score because borrowers with such credit files have a hard time getting loan approvals – if approved they have quite low negotiating power and pay very high-interest rates.

Below Average Credit Score:

It would still be difficult getting a loan and mortgage approvals with a below-average credit score. You may get a secured loan and secured credit card in Canada, but the interest rates would be higher. Research and opt ways to obtain good and excellent credit classification.

Fair credit score:

In Canada, your loan approvals won’t be a problem but interest rates would be higher than those falling in the good and excellent credit sets. You can get sanctioned for several credit cards except for premium cards; for which you have to mend your credit habits.

In Canada the average credit score is 667.

Good Credit Score:

You will be getting easier loan approvals and much better interest rates. A little effort and mindful credit utilization strategies; and you can unlock better interest rates and card rewards for yourself!

Excellent Credit Score:

Be ready for these perks, mate!

- Stress-free auto and mortgage financing approvals

- Best interest rates

- Higher loan limits

- Fine reputation

- Rewards, promotional rates, and bonuses on credit cards

- Premium credit card approvals

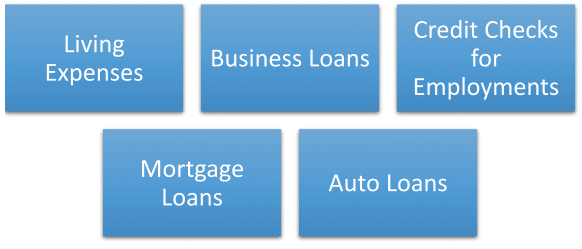

Why Credit Score Matters?

-

Living Expenses

If you have been managing home expenses for some time, you are aware that utilities like internet, electricity, phone service providers, television, and cable; are user available after credit checks.

If you own a good credit score, these services are readily available and utility companies won’t demand the security deposits.

-

Business Loans

Business startups require loans as additional capital apart from personal savings. To get approved for business financing, some crucial factors are:

- Business Plan/ Strategy

- Collateral

- Annual Revenue – sales and cash flow situation

- Credit Score

-

Credit Checks for Employment

Some employers check applicant’s credit reports prior to hiring. Some of the many grounds of doing so could be:

- Considering bankruptcies and late bill clearing as sore points

- Whether the salary being offered is comparable with their debt situations

To pass this background check and get employed in your ideal organizations, you gotta maintain a fine credit history!

-

Mortgage Loans

Your payment history influences greatly whether or not you would be accepted for mortgage loans and what interest rate will you be paying.

-

Auto Loans

If you have a poor credit score, you will be having only a few lender options to choose from. Plus, they would be charging you extremely high interest rates thereby increasing the actual value of the vehicle.

The same is the case with car insurance companies, their policies, and the charges.

What Activities Adversely Affect your Credit Score?

As a responsible borrower and a person in general, you need to know what may hurt your credit history and how you may avoid/ treat these dynamics wisely:

Applying for Several Cards in Short Span |

|

Deed in Lieu |

|

Closing a Card Account |

|

Credit Mix/ Credit Diversity |

Credit diversity accounts for 10% of your credit score. If you plan/ strategize a good mix of loan installments, credit cards, and other credit lines – this factor can raise your credit score. |

Co-Sign |

|

Credit Utilization |

Experts advise keeping this ratio to 30% of your credit limit. Spending more than 30% hurts your credit score. The lower the ratio, the better for your credit score. |

Credit Reporting Errors |

|

Faulty Payment History |

|

What are the Negative Items?

What does it mean that your credit file has negative items? Well, these entries reflect that you have not been responsible for your financial obligations. The presence (or absence) of these items reveals whether (or not) you are a high-risk borrower.

- Collections

- Bankruptcies

- Evictions

- Foreclosures

- Missed or late payments

- Repossessions

- Other financial maladministration pieces of evidence

These are some of the many negative items and stay on your credit file for quite a while.

Since lenders want the assurity that if the debtor would be able to pay the money back, and whether or not his lifestyle can afford this borrowed amount – they review the potential pledger’s credit file.

How Long Do Negative Items Stay on Your Credit Report?

Fair Credit Reporting Act (FCRA) is a federal law that governs the duration between which negative items linger on your credit report. Some like late payments remain for seven year while others like bankruptcy are taken off after ten years from your credit file.

-

Student Loan Default

Remain on your credit report for seven years.

Promissory notes in student loans specify timelines (which vary with the student loan categories) and if you miss these, this is when you should be ready to suffer the consequences of student loan default. It’s important to keep abreast of your student loan debt and you can calculate potential debt with the SoFi student loan pay-off calculator.

- In the case of private loans, you may contact the lender to communicate your situation.

- Department of Education can assist you regarding consolidation, loan rehabilitation, and repayment in case of provincial loan.

- If you have a limited (to nil) credit history, responsible managing student loans can boost your credit score.

-

Lawsuit or Judgment

Remain on your credit report for zero years.

Lawsuits and Civil judgments remained on the credit report for seven years in old times. Today, credit reporting agencies like Experian no longer file such damages.

Experian, Equifax, and Transunion undertook this change in 2018.

Since the above-stated credit reporting agencies have officially removed civil judgments of the credit report – you may ask to remove these if you discover their presence in your public records.

-

Delinquency/ Late Payments

Remain on your credit report for seven years.

If you fail to pay the bills 30 days late, these are reported on your file and remain for as long as seven years. Delinquencies are some of the primary negative items that harm your score.

To sidestep such damages, try to clear bills on time. Apps like Prism, Mint, and Personal Capital help to track bills and budgeting in Canada.

-

Foreclosure

Remain on your credit report for seven years.

In case the lender takes ownership of your property when you are unable to pay the mortgage loan, this situation is called foreclosure.

It may take your credit score down by 100 points. The greater the score, the high would foreclosures adversely impact your credit rating.

-

Charge off

Remain on your credit report for seven years.

When the lender misses so many payments, the creditor stops you from charging the account more. And your account is labeled as “charged-off.” The borrower is still liable for the debt thus taken.

Charge offs leave your file seven years after the delinquency date – the date of missed payment that led to charge off. Therefore to improve your credit score, ensure timely bill payments.

-

Bankruptcy

A Chapter 13 bankruptcy (also called a wage earner’s plan/ a repayment plan) remains for seven years.

A Chapter 7 bankruptcy (also called a straight bankruptcy) remains for ten years.

It may damage your score by 130-150 points. You may not be able to make any hard inquiry but getting and maintain a secured credit card would be a good option to rebuild your credit situation. Why secured credit cards because they don’t demand a good credit score but only a deposit for security.

-

Tax Lien

Remain on your credit report for zero years.

To secure the payments of tax (debt), a tax lien is the lien government has imposed to own personal or real property if you don’t clear your tax debt.

All credit reporting agencies have removed tax liens from credit reports now (like civil judgments).

If you find any tax liens on your credit file, contact bureaus to request their removals.

Is Removing Negative Items before time Possible?

Yes, only if the negative items thus stated are false.

The facts (late payments, bankruptcies, etc.) stay on the credit file till said time. However, if the stated info is erroneous you have a right to file a formal dispute with credit reporting agencies – since you would not want the wrong data spoil your credit information and eventually your credit score.

Repair has four phases:

- Data collection

- Analysis

- Evidence gathering

- Disputes

You may do it on your own or hire a professional to deal with bureaus, lenders, and collection agencies on your behalf. Experts know the procedures and can do the task quicker and efficiently comparatively.

How Long Does Positive Information Remain on Your Credit Reports?

Timely rent/ auto loan/ card payments are considered positive information.

Such info stays on your credit report indefinitely. In case you close your positive account, still, this positive info rests on your credit file for as long as ten years.